Partner Content

We asked our friends at Juno to share their wisdom on financing the MBA. Nicolas Echegaray, Wharton MBA 21’ and Juno’s General Manager, shared the following to help recent MBA Admits better prepare for their upcoming programs.

If you haven’t done so already, consider joining Juno’s MBA student loan negotiation group (free and no commitment). We use group bargaining power to get the best deal possible on your student loans! Join here for early member benefits.

What to Consider When Financing Your MBA in 2024

By Nicolas Echegaray, Wharton MBA ’21

First of all – congrats! I was in your shoes not so long ago. Five years ago, I was ecstatic when I received the admit call from my dream school.

If you are like me, after a few days of celebration, the next thing that comes to mind is how am I going to pay for this. In this post, I will reveal what I wish I had known before and the lessons I’ve learned working in the student loan industry.

None of this should be taken as financial advice.

Maximize free sources

First, the obvious. Find scholarships, grants, fellowships, and other free resources that can reduce the price tag on your degree.

By far, the largest amount of scholarships (for most MBA schools) are awarded at the point of admission. There are two main types of scholarships given by schools (not all schools give both): need-based and merit-based.

Need-based scholarships are based on your personal financial situation and the school’s assessment of your financial need. If you were earning a good salary prior to business school and don’t have dependents, chances are you will receive less than someone earning a fraction of your salary and coming to the school with their family.

Merit-based scholarships are based on your school’s criteria. Merit could mean multiple things: School assessment of the strength of your profile, some specific fellowship that targets a specific demographic (e.g. Forte Fellowship for women), etc.

Schools have some discretion on how these funds are allocated, and some schools may be open to negotiating scholarship offers if you can provide them with a strong reason (politely!).

Just be candid and honest about your situation. Bonus points if you have an offer from a peer school that includes a bigger scholarship!

Remember – they won’t take away your admission offer just for asking, but be polite!

Weigh whether to use your personal funds

If you are in the fortunate position of having savings – congrats! Having savings will give you flexibility. These are the things I’d encourage you to consider:

- Keep an emergency fund: You should always have money for a rainy day. You also don’t want to end up with nothing in your bank account at the end of the program.

- Consider the return on your investments. If you are investing in assets that you expect will return higher (after tax) than the cost of your loans, it may be worth taking loans even if you have the cash on hand.

- Make a realistic budget. Unfortunately, most MBA students end up spending more than their school’s published budgets. We have a tool with some historical information here. Consider your unique circumstances and what you want to get out of the MBA.

- Finally, consider the cost of your loans! We have seen some Juno members getting rates below what the money market or high-yield savings accounts pay, so they actually made money by taking a loan.

If you’re looking for a good option for this, take a look at Juno’s negotiated Savings Account option that gives you a 5.25% APY + an extra 1% cash back bonus on your deposit, exclusive for our Super Early Members. Note that this deal is available for a limited time and that terms and conditions apply.

Student Loans

The next most common piece of the funding puzzle is student loans. The options differ significantly depending on whether you are a domestic or international student.

Domestic Students

If you are a US Citizen or a Permanent resident, you have two main providers of loans: the US Government and Private Lenders.

Federal Loans: These are loans originated by the US Government. They are standard – all the students who qualify get the same terms, independent of individual credit scores. Federal Loan rates are fixed (with no option for a variable rate), whose rate is set annually in May. This rate does not fluctuate for the life of the loan.

The Federal Loans available for MBA students are:

- Unsubsidized loans: Up to $20,500 per year and with a ~1% origination fee

- Grad PLUS loans: Up to the Cost of attendance and with a ~4.2% origination fee

Federal loans come with certain perks, such as the potential for forgiveness if you work in public service for a number of years or special payment plans if you are unemployed. They’re definitely worth considering, depending on your specific profile and goals.

Private loans: These are loans made by a private company and are underwritten to your specific credit profile. A student with a strong credit history will likely have a better rate than someone with a poor one. Moreover, they allow the opportunity to add a cosigner (if you desire so) that can potentially improve your rate even further.

Most private lenders do not charge an origination fee. The main cost to focus on is the interest rate.

People should only consider private student loans if they are cheaper than their Federal loan alternatives (if the total cost is going to be the same or more, it’s usually better to stick with Federal).

Special consideration: Consider that you may end up paying your loans faster than the standard schedule. Some students focus only on the interest rate when comparing Private vs Federal Loans and disregard the origination fee. This fee can substantially add to the cost of the loan, especially if you are likely to refinance or pay your loans ahead of schedule.

International Students

The student loan market works differently for international students. On one hand, they are not eligible for Federal loans. On the other, they are (in most cases) not eligible for the same Private Lenders as domestic students.

That leaves international students to choose between a few options; our main recommendation is to explore all so they can get a complete picture:

Specialty lenders: there are a handful of lenders that offer loans catered towards international students. Unfortunately, their rates tend to be significantly higher than what domestic students can get. Also, these lenders may have origination fees and caps on how much you can borrow (typically less than the cost of attendance).

Home-country lenders: There are a handful of countries that have local lenders that offer student loans. Many of them require an asset as collateral (e.g. a house). In addition, if your goal is to stay in the US after your program, you may face some limitations in the future (for example, difficulty refinancing them).

School-based lenders: Some schools have agreements with certain US lenders that offer a special program to their students. Unfortunately, very few schools have these programs. Ask your financial aid office, or shoot us a note, and we can tell you if we are aware of one! Usually, the most affordable way of getting a loan for an international student is through a cosigned loan. A US cosigner is a US Citizen or Permanent Resident currently making an income who has an adequate credit history willing to guarantee your loan.

A little about Juno

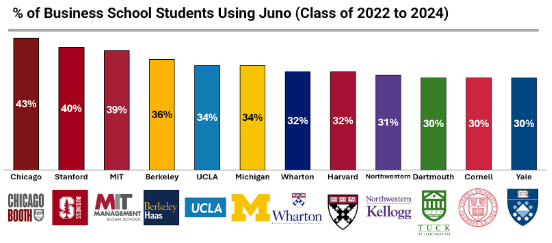

If you are not familiar with us, we are a group bargaining organization that negotiates more affordable student loan rates with lenders; we started out of Harvard Business School and have done it for the past six years. Many MBA students become members:

This year is a uniquely challenging environment, as rates have gone up significantly. We are currently negotiating with multiple lenders to make sure we get you the best possible loan in the Fall.

Here’s how it works:

- From now until April 30th, MBA students join the group.

- In May, we get final bids from banks and credit unions who want to serve the group. Then, we select the most competitive offers based on who provides the lowest rates.

- In June, we will make those offers available to you.

Our sincere request is to join our group and tell your friends. It’s free to join; there is no commitment, and we are working hard to bring you the best deal we can find in the market.

Finally, you are not alone.

An MBA is an incredibly rewarding experience. If you have already made the decision to attend, focus on the things you can modify (finding scholarships and good financial planning), and do not stress over the ones you can’t.

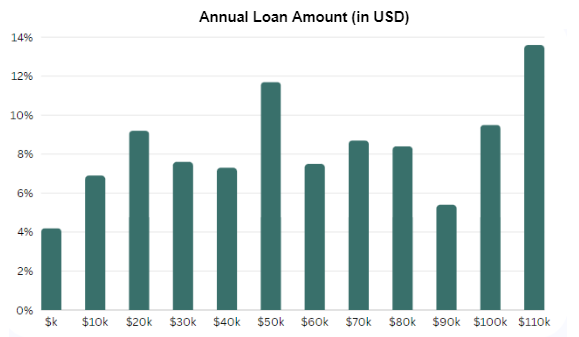

Many students need to take loans to cover tuition; ~13% of Juno members borrow the full cost of attendance.

I wish you the best in your endeavors! Feel free to reach out if you want to chat. We are rooting for you!